New rules help borrowers compare home loans and see the total cost before closing

Illustration: Chris Gash

By: Anya Martin

September 30th, 2015

Mortgage borrowers should find it easier to compare different loan products and understand the total cost of their loan under new rules that take effect Saturday.

The changes are part of the Consumer Financial Protection Bureau’s “know before you owe†initiative. And while the feedback has been generally positive, some real-estate professionals worry that new waiting-period rules could hurt some home buyers.

Here’s a breakdown of the changes.

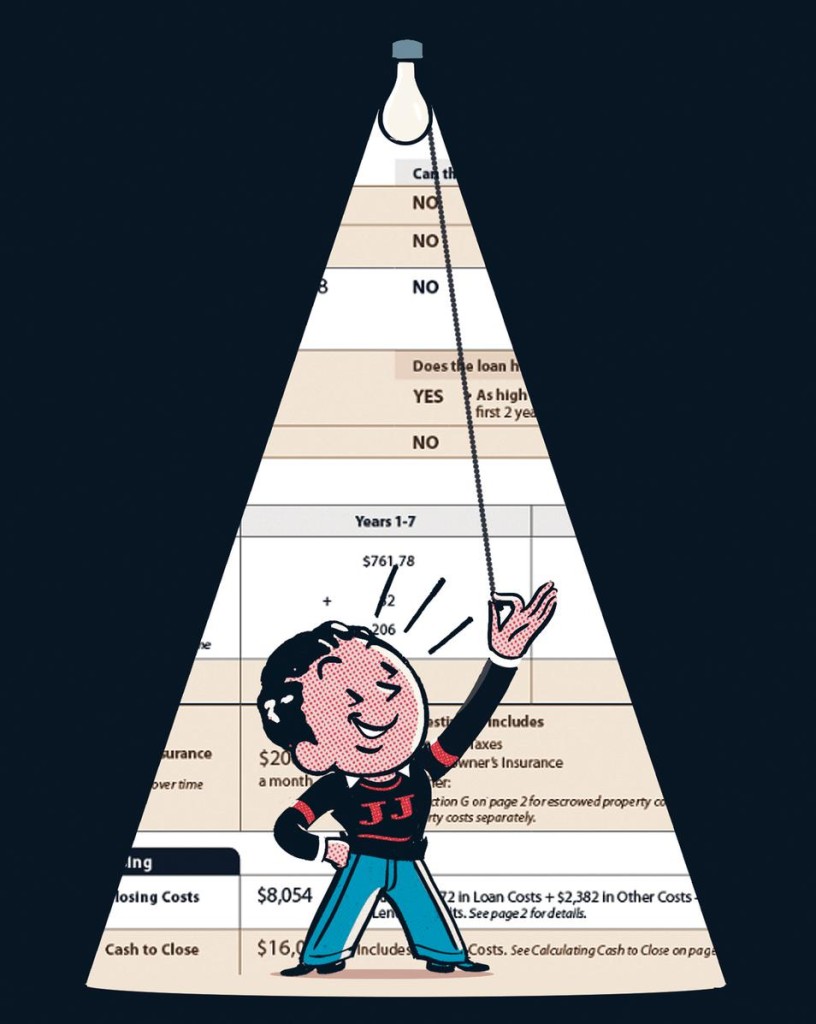

First, four documents are reduced to two. The Loan Estimate, provided by the lender at the time of mortgage approval, will replace two documents, the Good Faith Estimate and initial Truth-In-Lending Statement. The Closing Disclosure, provided by the lender just before the closing, will replace the HUD-1 Settlement Statement and the final Truth-In-Lending Statement. “There’s literally no way to even compare the [old] Good Faith Estimate and the Loan Estimate,†says Bob Kelly, an executive with Bank of America. “The document has taken on such a dramatic change, but the changes are very consumer-friendly.â€

Consumers can now easily check whether the loan amount, interest rate, monthly payment, escrow sum and the amount that a borrower needs to bring to the closing (a new feature) have changed from the lender’s initial estimates, Mr. Kelly says. The Loan Estimate also itemizes all closing costs and notes which services a borrower can shop for, such as title-search company and pest inspector.

The third page of the Loan Estimate includes information to help a borrower better understand the long-term costs of the loan. One new feature looks ahead to what the borrower will have paid in principal, interest, mortgage insurance and other loan costs at the five-year mark.

To help with comparison shopping, the Loan Estimate details the annual percentage rate (APR), so a borrower can put documents side by side and compare overall costs easily between loan products, such as a 15-year and 30-year mortgage, says Mathew Carson, a mortgage broker with San Francisco-based First Capital Group. The APR factors in not just interest rate but mortgage-broker fees and closing costs.

The Loan Estimate also shows the total interest percentage—the total amount of interest that you will pay over the loan term as a percentage of the loan amount.

The Closing Disclosure also is more user-friendly than the documents it replaces. For example, escrow costs are itemized to show what portion of the payment goes toward homeowner’s insurance, mortgage insurance, interest and taxes.

Overall, borrowers are going to have a much clearer notion of how much they will owe at closing and throughout the lifetime of the mortgage, says John Walsh, president of Milford, Conn.-based Total Mortgage Services. “The forms are much less confusing and more concise.â€

Still, one rule change concerns some lenders, agents and title insurers: waiting periods. The CFPB mandates three business days for hard copies of the Closing Disclosure to be received by mail and reviewed for any issues or errors by the borrower. If no issues arise, the closing can take place three days later. This rule applies even if a lender electronically sends or hand-delivers the documents.

In most markets, the additional days should not affect home buyers and lenders, Mr. Kelly says. Bank of America expects to still close mortgages within 30 days or less and has been providing seminars for real-estate agents to encourage them to move up property home inspections, property walk-throughs and anything else that could raise issues that must be addressed before closing, he adds.

Late changes in the terms of the loan, such as a switch from a fixed-rate loan to an adjustable-rate loan, may require a new Closing Disclosure form, further delaying the closing. That gives the home buyers time to decide what impact the new terms will have on their finances.

However, in competitive real-estate markets such as Portland, Ore., any extra delay could hurt borrowers vying in bidding wars with cash offers, says Shannon Baird, a broker with Portland-based Meadows Group Realtors. “Cash buyers are going to be stronger than they already have been,†she adds.

The CFPB emphasizes that the disclosure form and waiting period are designed to help borrowers pick the best loan for their situation.

“From the consumer perspective, the [new rule] could even take some angst away,†says Mr. Kelly. “You’re going to know a week in advance if you’re going to close.â€

Published by